Understanding Zakat and Sadaqah

-

What is Zakat?

-

Zakat is the third of the five pillars of Islam. It is an Islamic concept that seeks to bridge socioeconomic gaps through the transfer of a certain portion of money from the wealthy to those that are in need. The broader aim of Zakat is to eradicate poverty and promote self-sufficiency. For a detailed explanation please see The National Zakat Foundation.

Zakat should be paid as soon as possible as it is an immediate obligation for all Muslims. Only when there is a valid reason can it be delayed. Once Zakat has been transferred, it becomes the full ownership of the recipient and no longer the property of the donor.

- Am I required to give Zakat?

-

According to Shari’ah teachings, Zakat is required to be paid by Muslims if a person is: 1. Adult (having reached the age of puberty) 2. Sane 3. In complete ownership of the ‘Nisab’.

- What is the Nisab?

-

The Nisab was set at a rate equivalent to 87.48 grammes of gold and 612.36 grammes of silver. Today, silver and gold are not used as monetary exchange, so when calculating Zakat, the donor needs to find out the equivalent of the rates in the currency they wish to use for their donation. This can be done by checking the market rate of gold and silver.

Zakat is applicable only on net assets equal or exceeding the Nisab threshold. If a Muslim only has gold as an asset, then the Nisab measure for gold is used. If he/she has a mixture of assets, then the Nisab level for silver is used. This means that if net assets (income and savings) are above the silver Nisab threshold, Zakat would be applicable on the total amount of wealth owned.

- When do I pay My Zakat?

-

The Zakat year begins on the date wealth equals or surpasses the Nisab; Zakat should then be calculated and paid after one lunar year has passed which is the ‘Hawl’. Annually, Zakat should be paid on this date. If the donor cannot remember the date they first became owner of the Nisab, then the date should be estimated. If this is not possible, then any Islamic date should be selected arbitrarily and adhered to annually. This is referred to as the ‘Zakat anniversary’.

- Who is eligible to benefit from my Zakat?

-

With reference to the recipient of Zakat, the ‘Shari’ah’ addresses a number of spiritual, societal, political, and individual goals. In essence, Muslims are required to give a little from a lot, and in doing so, not do themselves any financial damage whilst providing security for those in need.

There are eight categories of people to whom Zakat can be distributed: 1. The poor; 2. The needy; 3. Administrators of Zakat; 4. those whose hearts are to be reconciled; 5. Travelers who left their homes for a lawful purpose and for whatever good reason do not possess enough money to return home, even if they are rich in their own country; 6. Muslims under bondage/slavery; 7. Muslims in debt; and 8. In the cause of Allah (this channel covers promoting the Islamic value system).

- How do I calculate my Zakat?

-

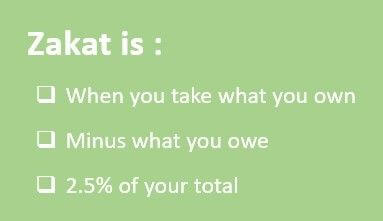

You can calculate Zakat on HasanaH using the Zakat Calculator. Zakat is compulsory on the following wealth criteria: 1. Complete ownership; 2. Wealth with ability to grow and increase; 3. Wealth that has reached the Nisab; and, 4. A full lunar year passes after possessing the Nisab. Zakat is calculated using a simple formula by subtracting deductible debts from ‘Zakatable’ assets. If the resulting figure is above the Nisab, then a Muslim must pay 2.5% of that figure as Zakat.

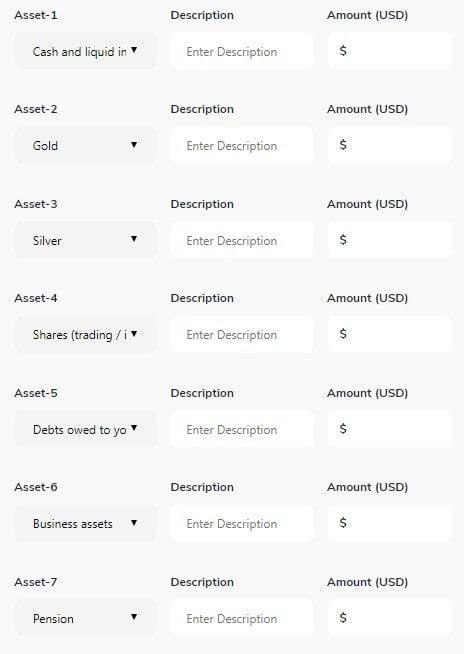

My ‘Zakatable’ assets

Gold and silver - All forms of gold and silver, e.g. jewellery, coins, are subject to Zakat. The Hanafi school treats all gold and silver jewellery as ‘Zakatable’, regardless of whether it is worn or stored. The resale value will be used to determine its worth. Other schools of Islamic law do not consider personal worn gold and silver as ‘Zakatable’.

Cash and receivables - All forms of cash, e.g. in a bank account, wallet, net rental income, or even under the mattress, are ‘Zakatable’. Cash that was lent to others and debts owed to the owner from any business activity are also ‘Zakatable’.

Shares, unit trusts, and equity investments - If shares are purchased with the main intention for resale, then the entire shareholding is ‘Zakatable’ at the current market value. However, if shares are purchased as a long-term investment to generate dividends, then Zakat is only due on the net ‘Zakatable’ assets of the company. This can be calculated from the company’s annual balance sheet.

Pension - Defined contribution schemes are ‘Zakatable’ whereas defined benefit schemes are not. For defined contribution schemes, Zakat is only due on the ‘Zakatable’ assets in the pension fund. Zakat is calculated by determining the percentage of ‘Zakatable’ assets in proportion to the pension pot value. Then, 2.5% of that net figure is the Zakat due on the pension. If the portfolio consists only of equities, it is advised to take 40% of the current market value of the portfolio as a proxy and then pay 2.5% of this figure. Rental property in a pension fund is not ‘Zakatable’ regardless of the percentage.

Stock - Anything purchased with the intention to resell is ‘Zakatable’ and is to be valued at its sale price.

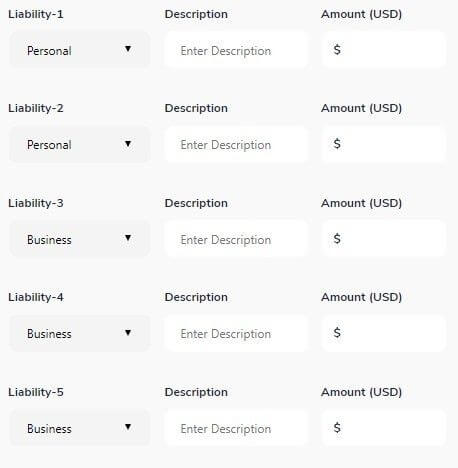

My deductible liabilities

Personal liabilities - Debts that are due or outstanding for repayment on one’s Zakat anniversary are deductible liabilities. Whereas debts in relation to future bills, eg. rent, utilities. For long-term debt, eg. mortgages, or student loans, the non-interest or capital amount can only be deducted for the forthcoming lunar year. However, it is recommended that this deduction is only made if one fears the inability to repay the debt as a result of not making the deduction.

Business liabilities - Certain short-term and long-term liabilities are deductible assets: 1. The total value of rent, bills, and salaries outstanding or overdue; 2. The total value of outstanding short-term commercial loans; 3. The next year’s non-interest portion of long-term business debt; and, 4. The total value of goods purchased on credit.

-

What is the difference between Zakat and Zakat al Fitr?

-

Zakat al Fitr (or Sadaqat al Fitr) is a duty that is paid on the occasion of Eid al Fitr and is required of every Muslim.

The head of the household may pay the required amount for the other family members.

It is advisable to contact your local mosque and get them to give you the recommended amount to pay per member of the family.

The first difference between Zakat and Zakat al Fitr is eligibility: 1. All Muslims must pay Zakat al Fitr regardless of their age or financial status (unless they honestly do not have the means to do so); 2. The amount attributed to Zakat al Fitr is very small, and rarely exceeds £5. Zakat, however, can amount to a larger number because it is 2.5% of all net savings; and 3. Zakat can be paid at any time, with the only condition being that the earnings reflect one year’s worth of net savings (one lunar year). Zakat al Fitr, however, goes hand in hand with Ramadan. Zakat al Fitr is paid during Ramadan before the month ends. It needs to be paid before the Eid prayers at the very latest.

-

What is Sadaqah?

-

Sadaqah is a voluntary form of Muslim giving with no time limits or threshold of wealth considered. Sadaqah is an act of worship with no conditions, and can be distributed to any cause the donor sees fit.

Islamic philosophy greatly appreciates the value attached to Sadaqah. This is further reinforced by the fact that Islam does not confine Sadaqah to financial help. Kindly actions and good deeds done by one person for the benefit of another are considered in the same light. The term is used in ordinary speech by all people to refer to any good and kindly deed.

Sadaqah is sometimes used interchangeably with Zakat. Indeed, it is the term used to refer to Zakat in the Quranic verse enumerating the categories of deserving Zakat recipients. However, Sadaqah is a more general term than Zakat, because the latter denotes an amount of property that a Muslim is required to give as a fundamental requirement towards social good.

-

Does HasanaH follow the official opinion of one or more of the four schools of Shari’ah?

-

HasanaH is guided by Dar Al Iftaa’ Al Misriyah, which advocates for not restricting Muslims to a single school of Shari’ah.

-

Does HasanaH evaluate or accredit projects in its catalogue for Zakat compliance?

-

HasanaH does not evaluate or accredit projects for Zakat or Shari’ah compliance. The donor on HasanaH is the ultimate decision maker on whether a specific project satisfies their beliefs regarding its compliance with Quranic scripture and the different Shari’ah interpretations.

-

Can Zakat funds be used to cover expenses (operational, transfer, conversion etc) associated with the distribution of Zakat?

-

According to Dar Al Iftaa’ Al Misriyah and The General Authority of Islamic Affairs and Endowments in the UAE, donors can deduct the incurred transfer charges from their Zakat money. Some Shari’ah Schools allow for up to 12.5% to be deducted from Zakat by the ‘Carrier’ of Zakat.

-

Do any of the projects on HasanaH grant Sadaqah to non-Muslims?

-

Yes, and this is permissible according to Dar Al Iftaa’ Al Misriyah and The General Authority of Islamic Affairs and Endowments in the UAE.

-

Does HasanaH keep Zakat funds in an Islamic bank or an interest-free account?

-

HasanaH keeps all its funds in a non-interest-bearing bank account.

-

Does HasanaH record Zakat and Sadaqah donations separately since their respective distribution requirements differ?

-

No. This is up to the beneficiary organisations to implement as and where required.

-

Do any individual Zakat donations get pooled with other Zakat donations to serve a specific Zakat-relevant cause?

-

This would be determined by beneficiary organisations, and should be communicated by them accordingly.

-

Is it permissible to donate to projects outside of my place of domicile though HasanaH?

-

According to Dar Al Iftaa’ Al Misriyah, Sharia permits the transfer of Zakat to wherever it is most needed. Furthermore, some scholars encourage transferring Zakat to whomever is in graver need for it, especially for the purpose of saving lives.

-

Is it permissible to pay Zakat and Sadaqah to a mediator (be it HasanaH or an entity that is listed on HasanaH), which would determine and manage the allocation of money?

-

This is permissible, according to Dar Al Iftaa’ Al Misriyah.

-

Is it permissible to move Sadaqah from a Muslim country to a non-Muslim country for retention and pooling, after which the sum gets distributed amongst deserving beneficiaries around the world?

-

This is permissible, according to Dar Al Iftaa’ Al Misriyah, especially when such alms are needed for saving lives.

-

Is it permissible to partner with international non-Islamic organisations for the distribution of Zakat and Sadaqah, given that the distribution is in accordance with Shari’ah law?

-

Yes. This is permissible, according to Dar Al Iftaa’ Al Misriyah.

-

What is Shari’ah’s position on anonymous vs. public donating of Zakat and Sadaqah?

-

According to the General Authority of Islamic Affairs and Endowments in the UAE, donating in discretion is advised, unless its public display entails a more positive impact and is performed in utmost sincerity.

-

Does HasanaH require beneficiary organisations to publish proof that all obligatory alms are distributed to eligible Muslims without any loss, and to prove that operating expenses and wages associated with obligatory alms came from other sources?

-

Beneficiary organisations are responsible for their own compliance with these requirements, and can communicate about this in their project descriptions and consequent Impact Reports. Accordingly, donors will be informed and able to make giving decisions based on their own beliefs and preferences.

HasanaH and The Four Schools of Islamic Shari’ah

The Use of Zakat Funds

The Use of Sadaqah Funds

Banking and Registry of Zakat and Sadaqah Funds

Pooling Zakat Funds

Donating Internationally

Donating through Mediators

Donating in Discretion

Publishing Proof of Compliance with Shari’ah

*Definitions and Shari’ah interpretations are courtesy of Dar Al-Ifta Al-Missriyyah in Egypt and The National Zakat Foundation in the UK.